It's incredible! 📱

With Yaseen Rostom, founder & CEO of Incredible.

Hi everybody,

I'm happy to announce the launch of the Fintech Society’s WhatsApp Channel!

For the past few months, I've been sharing fintech news on LinkedIn. Now, I want to make it even easier for you to stay informed.

What could be better than receiving the latest news directly on your phone via WhatsApp?

Every Friday, you'll get a complete recap of the week's fintech news in Europe.

It's free, and it’s in preview access for the readers of this newsletter!

B2C is not an easy market!

As one of my previous guests said, it is wonderful when it works because it offers a real leverage, but it demands a lot of investments to develop the brand, to get a sufficient customer base, and to find a business model that fits.

Yaseen Rostom, founder & CEO of Incredible, definitely understands that.

It was interesting to talk about debt management, the importance of UX, and consolidation of the business model.

Enjoy!

⏱️ Reading time: 5 minutes

Hi Yaseen, what is Incredible?

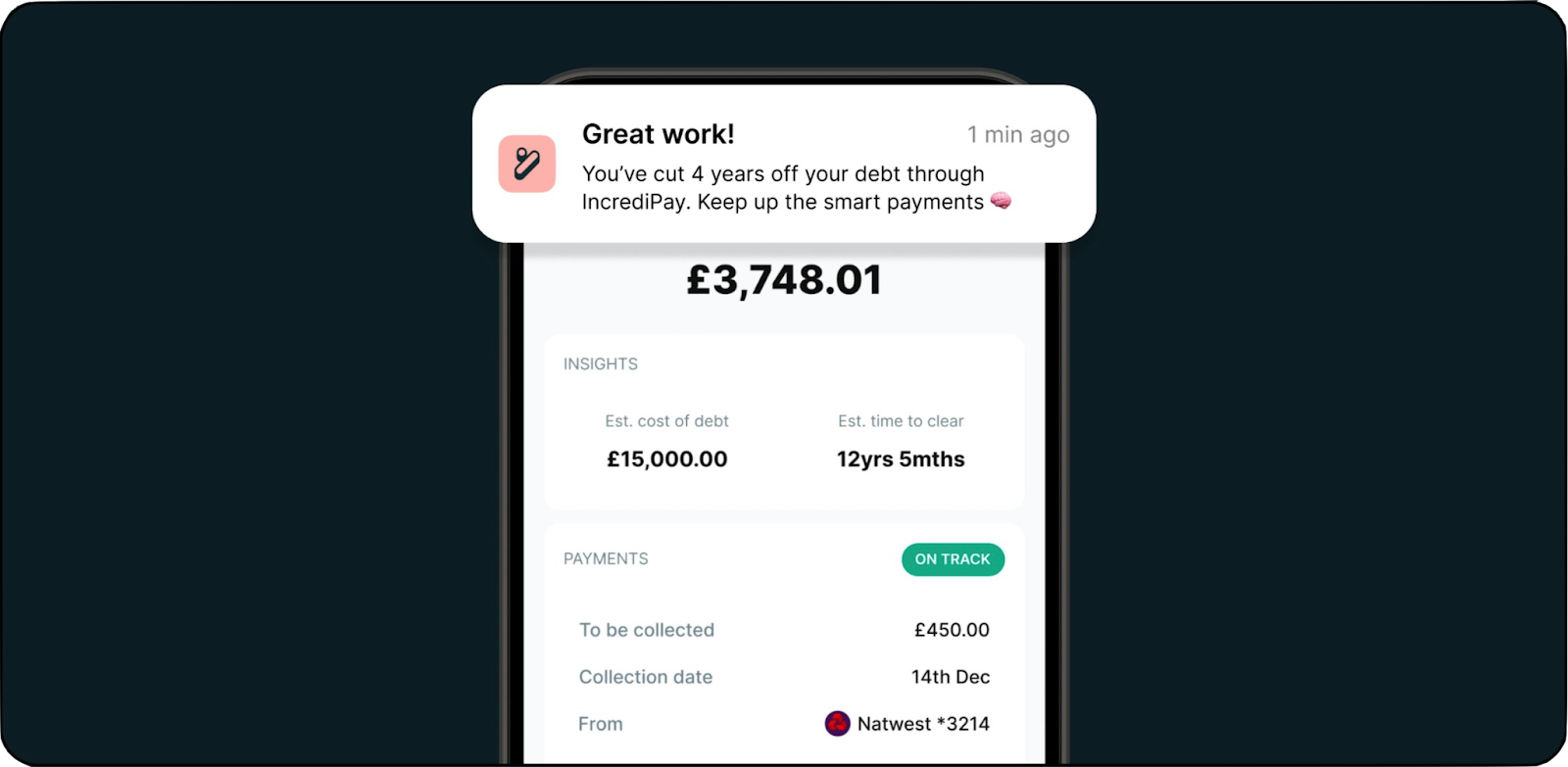

Hi Thomas! Incredible is a repayments platform for consumers. We allow consumers in the UK who are managing multiple sources of credit—such as credit cards, loans, and car finance—to automate their repayments into a single payment.

Currently, we focus on credit cards. If you have multiple credit products and credit card payments coming out throughout the month, we consolidate these into the most efficient payment method. We optimize this process based on your balances, interest rates, due dates, and other factors to ensure the most cost-effective repayment.

Do you use credit cards in the UK? Because in France, debit cards are the norm.

Generally, credit card usage in the UK is much higher than in most of Europe, where people tend to be more debt-averse.

Although the numbers in the UK are not as high as in the US, they are increasing. For the first time ever, consumer debt in the UK has reached 2 trillion pounds, with a significant portion of that on credit cards. There are roughly 54 million credit cards in issuance in the UK, and over 55% of those carry a balance month to month.

What are the main problems in the debt management market?

In the last 10 years of fintech, we've seen it become much easier to save and invest money automatically. You can buy shares in Apple faster than you can buy a phone. However, debt management has generally been ignored. Traditional debt management solutions are usually government-backed plans that rest on your credit file for six years, making it very difficult to borrow money again.

Other products may help you visualize your debt but provide shallow actions. They offer insights but don’t automate the repayment process.

Do you think we can access debt too easily with tools like Buy Now, Pay Later (BNPL), even if there are no interests?

Yes, there's a term called "phantom debt," where people don't even realize they're in debt. Much innovation in lending focuses on quick underwriting decisions and offering loans at the point of sale. BNPL can be beneficial in theory. It allows you to split payments with zero interest. However, it becomes problematic when used for everyday expenses like groceries and takeaways, leading to stacking multiple BNPL payments. People end up not knowing what they owe in 90 days.

Moreover, some people use credit cards to pay their BNPL bills, complicating their financial situation. We aim to bring transparency to the credit and debt ecosystem, so people understand their loans' costs and the best repayment methods.

In 2022, Simon Taylor (a famous fintech writer) praised your fintech's design and UX. Is this a major focus for you?

Absolutely. Design and user experience are central to what we do. If you search for debt management solutions, many haven’t been updated to meet modern consumer expectations.

Today, people are used to experiences like Spotify and Revolut. Even if it's a boring subject like credit and debt management, the experience needs to be engaging and user-friendly. This makes it easier for customers to manage their finances.

How do you ensure that the experience fits with consumer willingness? Do you have a feedback or iteration system?

Exactly. Throughout all our product variations, we always seek feedback from users. Before we had a product, we spoke to hundreds of people to understand their financial habits and needs. We incorporate this feedback into our development process, ensuring our products address real consumer struggles.

We set up analytics early on and continually review our processes. If a user reports an issue or deletes their account, we don't just fix it; we get them on a call to understand their concerns and improve our service.

When was Incredible launched?

We launched the first version of our app about 11 months ago and currently have just over 2000 users.

Are you only in the UK for now?

Yes, we are currently only in the UK. However, we plan to expand to other markets, such as Latin America or the US, in the next 18 months. Although we could launch in Europe, the levels of debt are generally lower compared to the US and Latin America.

What's the main learning you can share since the beginning of your journey?

The main learning is that it's about a hundred times harder than you think it will be. Despite all the advice and feedback you get, every founder has to go through their own unique challenges. You need to survive your mistakes to gain deeper insights into your market.

What's your business model?

Our business model is twofold. On one hand, we charge a transaction fee on the consumer side. On the other hand, we work with lenders to facilitate refinancing. We automate the refinancing process for both consumers and lenders.

B2C is not an easy market. What's your plan to scale and consolidate your business model?

Partnerships with large financial institutions are crucial. We don't want to rely solely on social marketing. By connecting with various providers, we aim to serve a subset of their customers that they can't currently cater to.

This multi-faceted approach involves working through partners and directly reaching out to customers.

What's your vision for Incredible?

Although we started with credit repayments, we see ourselves as an optimization layer on top of people's finances. We manage a sum of funds in an Incredible wallet and automate various financial tasks, like paying different cards and saving on interest.

We aim to integrate deeply into users' everyday lives. We want to automate financial tasks people don't want to think about, especially debt repayment, making it easier for time-poor, resource-poor customers.

Thank you, Yaseen, for this great discussion!