Fintech For Inclusion

With Thomas Courtois, CEO of Nickel.

Hi everyone,

Today, I’m sharing insights from my discussion with Thomas Courtois.

Thomas is the CEO of Nickel, an inclusive bank account. The fintech is a subsidiary of BNP Paribas, one of Europe’s leading banks and an amazing sponsor of Fintech Society.

In this edition, you’ll explore:

Nickel’s vision

How to be inclusive

Partnerships between fintechs

Enjoy the read!

Access to financial services is regarded as a catalyst for progress in seven of the UN’s 17 Sustainable Development Goals. According to the World Bank’s 2021 Global Findex report (the latest one), 76% of adults worldwide held an account with a financial institution or mobile money provider by 2021. This marks a significant rise from 51% in 2011.

Naturally, these figures vary widely by region. In high-income countries, the rate of financial inclusion peaks at 96% — 99% in countries like France. Yet, even in highly developed economies, a considerable number of people remain in vulnerable financial positions. Here, the question is not really about being unbanked but rather about being underbanked.

Is this where fintech steps in?

5 Minutes at Your Local Tobacconist

If you have a poor credit history, low income, or are a migrant, accessing reliable banking services at a traditional bank can be challenging.

It was from this issue that Nickel was born in 2014.

Our founders launched Nickel with the ambition of democratizing and simplifying access to payment accounts and associated services. The idea was to allow everyone to integrate more fully into society, as living without a bank account is extremely difficult in today’s world. That’s how Nickel, the account for everyone, came to life.

Nickel offers an accessible account for all, easy to open thanks to its presence in retail outlets like tobacconists and local shops. The concept is simple: an account, a card, and a bank identification number, all opened within five minutes at a local tobacconist.

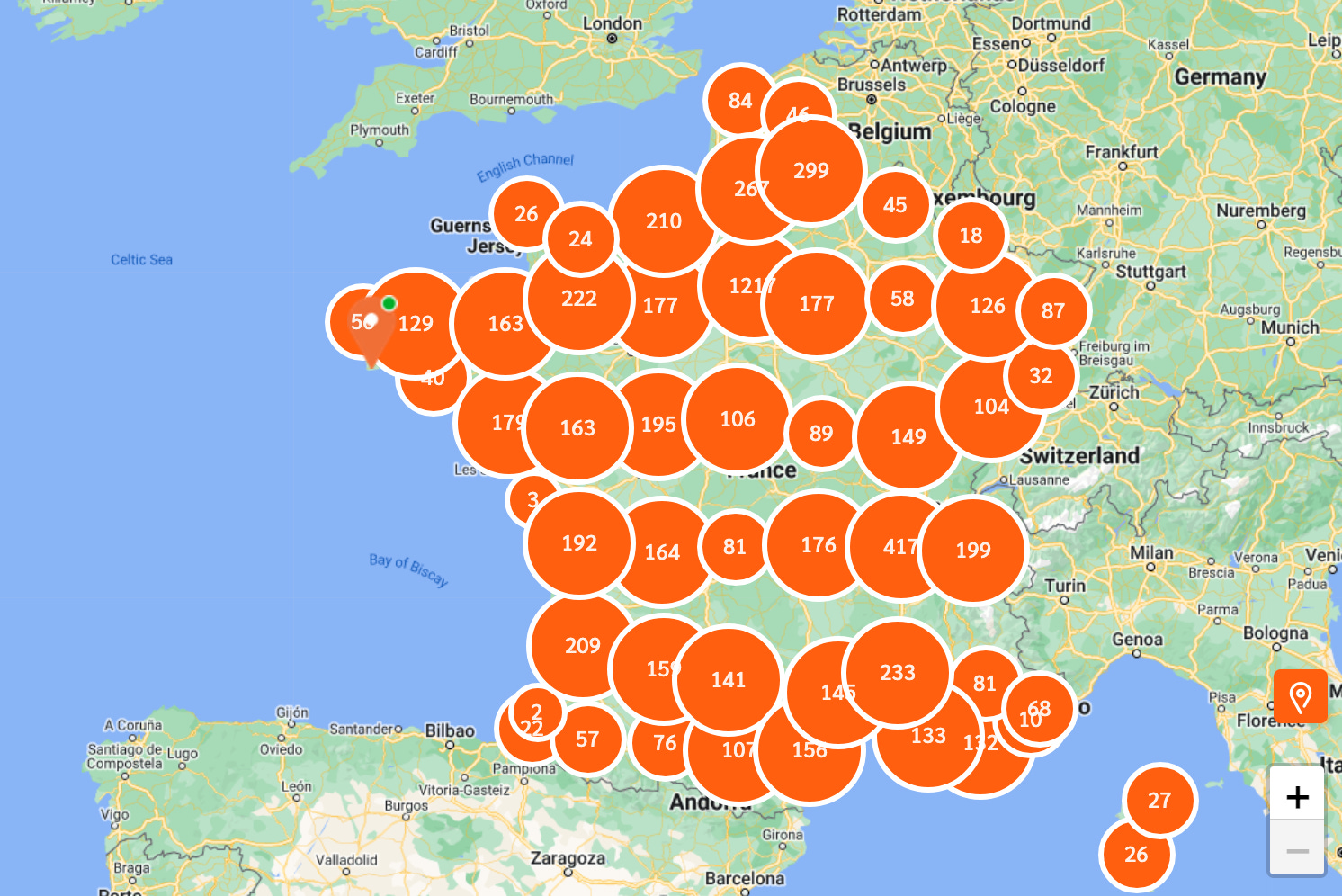

The fintech now boasts over 3.8 million customers and operates in 7,700 locations across France. Nickel has successfully broadened its appeal, expanding from its original target audience – those in precarious situations – to a wider customer base of individuals simply seeking a reliable product at a fair price.

Nickel meets a universal need and access to banking remains difficult in many European countries. This prompted the company to export its model. Just over three years ago, Nickel expanded into Spain, followed by Belgium and Portugal two years ago, and Germany last year. Today, one in four accounts is opened outside of France.

An inclusive model that is gaining ground.

How to Be Inclusive? (and The Challenges)

For the past decade, much of the discussion around neobanks has focused on fully digital customer journeys. It’s noteworthy how Nickel has taken a different approach, since its early days, by offering a physical account setup and management. A way to be more inclusive.

Today, we remain convinced that, to be truly inclusive and meet everyone’s needs, maintaining a physical presence is essential. It’s reassuring to know you can meet someone in person. It also allows us to provide local services, like cash deposits and withdrawals, or even an immediate replacement if you lose your card. We take pride in offering the best of digital banking with modern payment methods while maintaining a physical footprint across the country, where anyone can come to meet us and engage with us. Plus, walking into a tobacconist is far less intimidating than entering a bank.

I wanted to delve deeper into the topic of financial inclusion, which remains a complex issue in a highly regulated environment. To gain more insight, I spoke with Thomas about the different ways Nickel seeks to be more inclusive, as well as the challenges they face in doing so. Here are a few points.

First, simplifying account opening and offerings.

We ensure that our account opening process and offerings are easy for our clients to navigate. For instance, we accept over 190 types of identification documents, which is notably broad. Additionally, customers can seek assistance at a tobacconist when opening their account.

The complexity of regulation is, of course, a significant challenge. How do you maintain a smooth, near-instant experience when regulators require strict KYC procedures? The answer lies in leveraging advanced technology while also ensuring human oversight — one of the key elements of Nickel's partnerships with tobacconists.

This has been Nickel's expertise for the past 10 years. We’ve implemented technologies to verify a customer's identity during account setup, while ensuring a final face-to-face check at the tobacconist. We've also incorporated technology to ensure that all these checks are performed as quickly as possible.

Then, enhancing usability through UX and data enrichment.

When you review your transactions on the Nickel app, the merchant’s logo is displayed. You’ll also see the store’s address, its website if available, and a description of how you made the payment. Additionally, we were one of the first in France to introduce a tactile notch on our cards so that the visually impaired can easily orient them. We’ve also launched a customer service that’s accessible to the deaf and hard of hearing.

Finally, a critical factor, not only during the onboarding process but throughout the life of the account, is addressing the digital divide — an aspect that sets Nickel apart from neobanks.

We’ve always been committed to ensuring that you don’t need internet access or a smartphone to open a Nickel account. You can do so at a tobacconist using a terminal provided on-site. You can also manage your account via SMS banking — simply request your balance or your recent transactions through a text message.

For now, credit history isn’t a major concern for Nickel. Well, it is, of course, like it is for any payment institution — But Nickel’s real-time infrastructure ensures that clients won’t overdraw their accounts. And, “when you eliminate credit risk, you can naturally accommodate a broader customer base.”

But how long will this remain the case?

Partnerships Between Fintechs

For the average “payment institution” customer, the distinction between a credit institution and a payment institution is often blurred. To them, a payment institution is simply a bank, even if it lacks the status of a traditional credit institution. This leads to growing customer demands: “60% of our clients are using Nickel as their main account. They are asking for access to credit, savings, and insurance”.

But how should a payment institution respond to such demands? Should it prioritize partnerships, transform into a credit institution, develop these services in-house?

Nickel has chosen the path of partnership — partnering with FLOA for credit, for instance, or Lemonade and Cardif for home insurance.

The primary goal: speed.

I believe we would never have launched these services if we had waited to secure the necessary licences, develop the products, and learn how to manage them ourselves. There are already solutions in the market that work exceptionally well — some are even subsidiaries of our own group. So, we opted for partnerships to deliver the best possible offer to our clients. For example, with FLOA’s credit offering, it took us just nine months to make it available to our customers, whereas it would have taken at least two to three years to develop internally. And frankly, the customer experience would likely have been inferior.

Fintech is an intensely competitive market that revolves around a multitude of services. Partnerships provide a way to strengthen one’s position or enter new markets without engaging in overly direct competition. And who knows, such collaborations may even pave the way for mergers or acquisitions.